Company liquidation in the UAE is the legal closing of a business through an official winding-up procedure, not a casual decision to stop using a trade license. Just because activities have halted or the office has been evacuated doesn't mean the firm is officially closed. Obligations may nevertheless exist on paper and in law until the competent authority clears the entity and removes it from the register.

The process usually requires more than one internal and external step. Shareholders must approve the dissolution, a liquidator may need to be appointed, government and administrative clearances must be collected, employee matters must be settled, and tax and banking issues must be dealt with before the final de-registration stage can be completed. In practice, the difficulty is rarely in the idea of closing the company. The difficulty is in closing it cleanly.

This is exactly why liquidation in the UAE needs a structured approach. If the file is incomplete or liabilities remain unresolved, the closure can stall, costs can rise, and legal exposure can survive the business itself. This article breaks down the legal basis, the preparation stage, the procedural sequence, the cost factors, the hidden risks, and the role of professional support.

Legal Framework and Types of Company Liquidation in the UAE

Types of Liquidation

In the UAE, liquidation is the formal legal mechanism used to bring a company to an end in a recognized and enforceable way. It is the point at which the business stops existing as a legal vehicle, not merely as a commercial activity. From a practical standpoint, liquidation usually appears in two main forms: voluntary and compulsory.

- Voluntary liquidation begins inside the company. The shareholders, or the partners in the case of certain entities, make the decision to dissolve the business and start the winding-up process. This usually happens when the company has become dormant, completed the purpose for which it was created, or no longer makes commercial sense to maintain.

- Compulsory liquidation moves on a different track. It is driven by legal pressure rather than internal choice and is generally connected to insolvency, unresolved disputes, or judicial intervention. The difference is simple: one is chosen, the other is imposed.

The Role, Qualifications, and Legal Liabilities of the Official Liquidator

The liquidator is the person who turns the decision to close into a legally structured process. This is not a decorative appointment. In many UAE liquidation procedures, the liquidator must be an approved professional whose status is accepted by the relevant authority.

Their task is to review the company’s position, oversee the winding-up mechanics, deal with the documentation required for closure, and issue the reports needed for final cancellation. Because they operate at the point where finance, compliance, and formal closure meet, their role carries legal weight. If the process hides debts, skips liabilities, or relies on false records, the liquidator’s work becomes exposed to scrutiny along with the company itself.

Alternatives to Liquidation

Liquidation is not always the smartest exit. In some cases, a company can be sold, restructured, transferred to new owners, or reorganized before closure becomes necessary. Where the business still has value, liquidation may be the bluntest tool in the box.

But that only works when the company is still clean enough to move. If debts, regulatory issues, or unresolved staff matters are hanging off it, liquidation stops being an option of convenience and becomes the legal cleanup operation.

Preparatory Phase

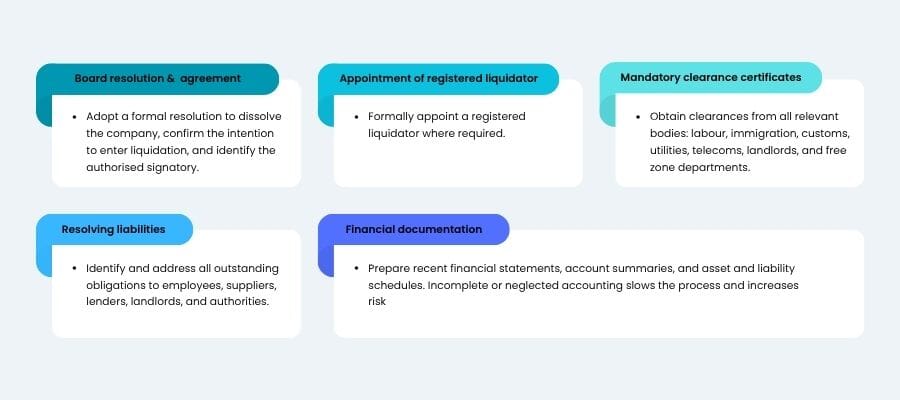

Drafting the Board of Directors' Resolution and Shareholders' Agreement for Dissolution

Before the liquidation process can move outward, it must first be authorized from within the company. That usually begins with a formal resolution adopted by the board or by the shareholders, depending on the legal form of the entity and its constitutional documents. This resolution records the decision to dissolve the company, confirms the intention to enter liquidation, and often identifies the person authorized to sign the required documents.

In companies with more than one owner, the shareholders’ agreement or equivalent corporate approval record becomes especially important. It helps show that the decision was made validly and reduces the risk of later disputes over authority, voting, or asset distribution.

Official Appointment of a Registered Liquidator and the Letter of Acceptance

Once the decision to dissolve has been approved, the company usually must appoint a registered liquidator if the applicable authority requires one. This appointment is not an afterthought. It is a formal legal step that gives the liquidation process its professional supervisor.

The appointment document is often paired with a letter of acceptance issued by the liquidator. That letter confirms that the appointee agrees to act in that capacity and is willing to carry out the work required for winding up the company in accordance with the applicable rules.

Mandatory Clearance Certificates

A UAE company cannot normally disappear from the register while loose ends remain open with other authorities or counterparties. That is why clearance certificates are a core part of the preparatory stage. Depending on the type of business and its place of incorporation, these may involve labour, immigration, customs, utilities, telecommunications, landlords, or free zone departments.

The point of these clearances is simple: they confirm that the company is not leaving unpaid obligations or active files behind. Missing even one certificate can delay the process disproportionately and force the company back into an administrative loop it thought was already finished.

Resolving Liabilities

No liquidation file is truly ready until liabilities have been identified and addressed. This includes amounts owed to employees, suppliers, service providers, lenders, landlords, and government authorities. The company must also assess whether there are pending claims, disputed invoices, contractual penalties, or obligations that have not yet fully matured but may still arise from past conduct.

This stage matters because liquidation is not designed to erase debt by magic. It is supposed to organize the settlement of obligations before the company is struck off.

Financial Documentation

A proper liquidation process depends heavily on reliable financial records. Authorities and liquidators may require recent financial statements, account summaries, details of assets and liabilities, and supporting records showing the company’s actual position at the time of closure.

Where the accounting is incomplete, inconsistent, or neglected for a long period, liquidation becomes slower and riskier. In plain terms, bad books make for bad exits. That is why preparing the financial file early is often the difference between a controlled closure and a prolonged administrative headache.

Step-by-Step Procedure for Liquidating a UAE Company

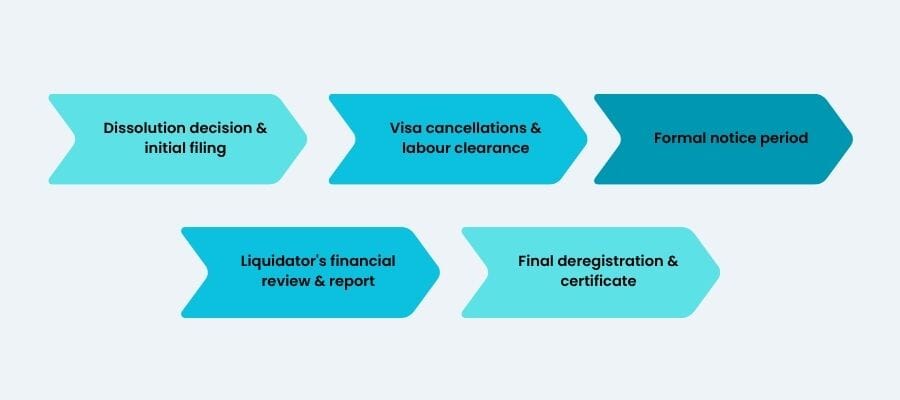

Once the preparatory work is complete, the liquidation process moves into its operational stage. Although the exact sequence can vary between mainland authorities and free zones, the overall logic remains broadly consistent. The company must pass through a chain of formal steps before the final de-registration certificate can be issued.

- The process usually starts with the adoption of the dissolution decision and the execution of the supporting corporate documents. Once that internal approval exists, the company files the initial application for liquidation with the competent authority. At this stage, the authority may request the resolution, constitutional documents, license copy, passport and Emirates ID details of the shareholders or managers, and the appointment documents of the liquidator where required.

- After the file is opened, the company generally proceeds with the cancellation of establishment cards, immigration records, and employee visas if these are still active. Labour files must also be regularized, and all end-of-service settlements or salary-related liabilities should be resolved before the process can safely move forward. If the company has customs registration, leased premises, utilities, or regulated sector approvals, these must also be closed or cleared with the relevant bodies.

- A formal notice period may then apply, especially where creditor protection is part of the applicable procedure. During this stage, the company effectively signals that it is entering liquidation and gives interested parties a limited opportunity to raise claims or objections. This is not a ceremonial pause. It serves a legal purpose and can affect the timing of the final closure.

- Parallel to these steps, the liquidator reviews the company’s financial position, verifies outstanding liabilities, and prepares the documents needed for the final report. Once all required clearances have been collected and all material issues have been addressed, the liquidator issues the liquidation report or closure statement in the form accepted by the relevant authority.

- The company then submits the final package for deregistration. If the authority is satisfied that the procedural steps have been completed correctly, the trade license is cancelled, and the company is removed from the register. That final certificate is the real finish line. Until it is issued, the company is often not as closed as its owners think.

Want to learn more about UAE business setup services?

Budgeting and Timelines

Government Fees

Liquidating a company in the UAE is never free, even where the business itself is inactive. Government charges usually arise at several points in the process, including license cancellation, immigration file closure, labour-related processing, publication requirements where applicable, and final de-registration. The exact amount depends on whether the company is registered on the mainland or in a free zone, as well as on the number of linked files that still need to be closed.

What catches many owners off guard is not one big fee, but the accumulation of smaller mandatory charges across different authorities.

Professional Expenses

In addition to official charges, most liquidation cases involve professional costs. These may include liquidator fees, legal drafting, document review, accounting support, tax deregistration work, translation, attestation, and coordination with multiple authorities. Where the company’s records are incomplete or liabilities are disputed, professional costs tend to rise because the closure stops being mechanical and starts becoming corrective.

A straightforward file may remain manageable. A messy one can turn into a billable archaeology project, with someone digging through years of neglected documents to make the company closable again.

Estimated Timelines

There is no single fixed timeline for company liquidation in the UAE because the speed depends on the authority involved, the condition of the company’s records, and whether tax, employee, banking, or creditor issues remain open. A relatively clean file may move through the process within a matter of weeks, while a more complicated one can take several months.

The main delays usually come from missing clearances, old labour or immigration files, incomplete accounting records, outstanding tax obligations, or slow bank closure procedures. Where a creditor notice period applies, that statutory window also extends the timeline automatically.

In practice, the fastest liquidations are not the ones with the most aggressive filing strategy. They are the ones prepared properly before filing begins. In this area, haste has a strange habit of making everything slower.

Hidden Pitfalls, Corporate Risks, and Post-Liquidation Liabilities

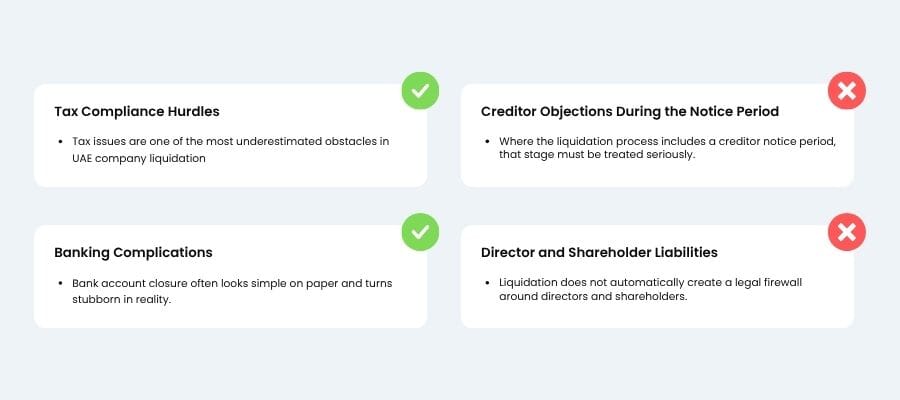

Tax Compliance Hurdles

Tax issues are one of the most underestimated obstacles in UAE company liquidation. Many business owners assume that if trading has stopped, the tax side will somehow fade out on its own. It does not. A company may still have pending VAT returns, unpaid administrative penalties, incomplete records, or corporate tax obligations that must be reviewed before deregistration can be completed.

Even where the business was inactive for part of its life, the tax file may still require formal closure. If the company was registered for VAT or fell within the corporate tax framework, deregistration must be handled correctly and supported by accurate records. A silent tax file is not always a clean tax file. Sometimes it is just a future problem wearing slippers.

Creditor Objections During the Notice Period

Where the liquidation process includes a creditor notice period, that stage must be treated seriously. It is the legal window during which creditors or other interested parties may raise objections, submit claims, or challenge the proposed closure if they believe the company still owes them money or has unresolved obligations.

This can delay the process significantly. Even a claim that is later disputed or settled may interrupt the expected timeline and force additional review by the liquidator or the competent authority. A company that enters liquidation before mapping its debts properly is basically inviting unpleasant surprises to arrive by registered mail.

Director and Shareholder Liabilities

Liquidation does not automatically create a legal firewall around directors and shareholders. If the company is closed with undisclosed debts, misleading records, unlawful distributions, unpaid employee dues, or regulatory breaches, liability may survive the company’s formal cancellation in certain situations.

This becomes especially sensitive where directors continued operating irresponsibly while the company was insolvent, or where shareholders withdrew value from the business without accounting for creditors’ rights. The legal entity may disappear from the register, but that does not always erase the conduct that took place before disappearance. A bad closure can leave a long shadow.

Banking Complications

Bank account closure often looks simple on paper and turns stubborn in reality. UAE banks may request updated corporate documents, board resolutions, proof of license cancellation steps, clearance evidence, and confirmation that there are no remaining liabilities linked to the account. If there are compliance flags, old KYC issues, dormant balances, or unexplained transactions, the closure can slow down sharply.

This matters because the liquidation process and the banking process often depend on each other. The company may need the account to settle final payments, but the bank may hesitate to close it until the liquidation is sufficiently advanced. That circular problem is more common than many owners expect, and it regularly becomes one of the last annoying stones left in the shoe.

Comprehensive Legal Support and Liquidation Services in the UAE

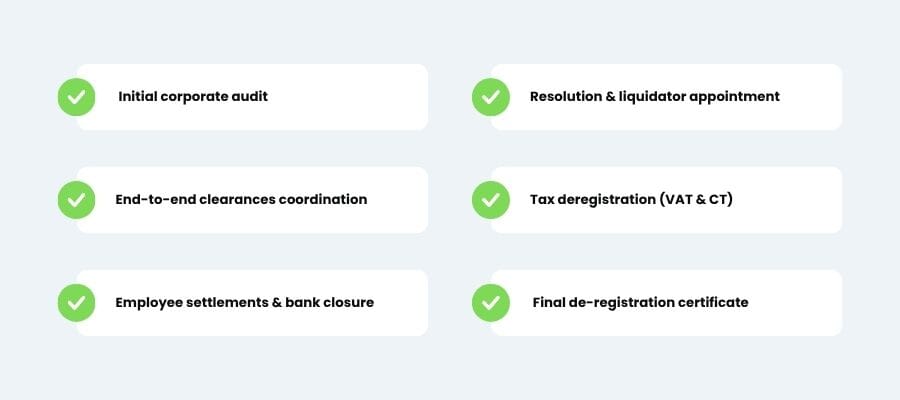

Initial Corporate Audit

Every successful liquidation starts with a proper diagnosis. Before any filing begins, the company’s legal status, licensing history, financial records, tax position, visa exposure, contractual liabilities, and regulatory footprint should be reviewed in full. This initial corporate audit helps identify what can be closed immediately, what needs corrective work, and where hidden risks may delay or complicate the process.

Preparing the Resolution and Appointing an Approved Liquidator for Your Company

A legally sound liquidation file begins with the right internal documents. Professional support is often used to prepare the board or shareholder resolution, align the wording with the company’s constitutional requirements, and ensure that the appointment of the liquidator is valid in form and substance. Small drafting errors at this stage can create disproportionate trouble later.

End-to-End Coordination for Securing Clearances (MoHRE, Immigration, Customs, Landlords)

One of the most time-consuming parts of liquidation is the clearance phase. Different authorities and counterparties operate on different systems, timelines, and documentary standards. Coordinated support helps the company collect labour, immigration, customs, landlord, utility, and other operational clearances in the correct sequence, instead of bouncing between desks like a corporate ping-pong ball.

Managing Complex Tax Deregistration (VAT & CT) and Interacting with the FTA on Your Behalf

Tax deregistration can become a separate project inside the larger liquidation process. Where VAT registration, corporate tax exposure, penalties, missing returns, or record gaps exist, professional assistance helps bring the file into a condition that the Federal Tax Authority can accept. This usually includes reviewing obligations, preparing submissions, addressing queries, and reducing the risk of closure being blocked by unresolved tax issues.

Assisting with Employee Visa Cancellations, Final Settlements, and Bank Account Closures

Employees, visas, payroll matters, and end-of-service settlements must be handled carefully during liquidation. Professional support can help ensure that labour-related obligations are settled in the correct order and supported with the right documentation. The same applies to corporate bank account closure, which often becomes more complex than business owners expect once compliance review begins.

Full Representation Before DED or Free Zone Authorities Until the Final De-Registration Certificate is Secured

The last phase of liquidation is where incomplete files tend to unravel. Full representation before the Department of Economy and Tourism, relevant mainland bodies, or free zone authorities helps ensure that follow-up requests, procedural comments, missing documents, and final approval conditions are handled without drift. The objective is not just to start the liquidation. It is to carry it through until the final de-registration certificate is actually issued.